新加坡汽车销量排名重新洗牌

你有没有想过,新加坡的汽车市场,在短短两年间,被一个来自中国的品牌彻底改写了? 那个被比亚迪攻陷的小红点 如果…

你有没有想过,新加坡的汽车市场,在短短两年间,被一个来自中国的品牌彻底改写了? 那个被比亚迪攻陷的小红点 如果…

在马来西亚,有三件事是绝对不可撼动的:国人的热情、椰浆饭里那勺没有妥协余地的参巴酱,以及永远在右车道闪着大灯逼…

先说一个真实的小故事。 广州中山八路有个做童装生意的伊朗商人,在国内待了十几年。早些年伊朗里亚尔兑人民币大概1…

在马来西亚,朋友或客户赖账不还?这篇文章带你了解从友好追讨到法律途径的完整方法,让你不再哑巴吃黄连。

想象一下,你花了五年时间,往一个巨大的存钱罐里拼命塞钱,塞进去足足有830亿美元——这笔钱足够买下整个法拉利、…

在1982年的纽约出租车里,有个司机载了一名乘客,当司机得知乘客来自法国时,他瞬间两眼放光。”哦!…

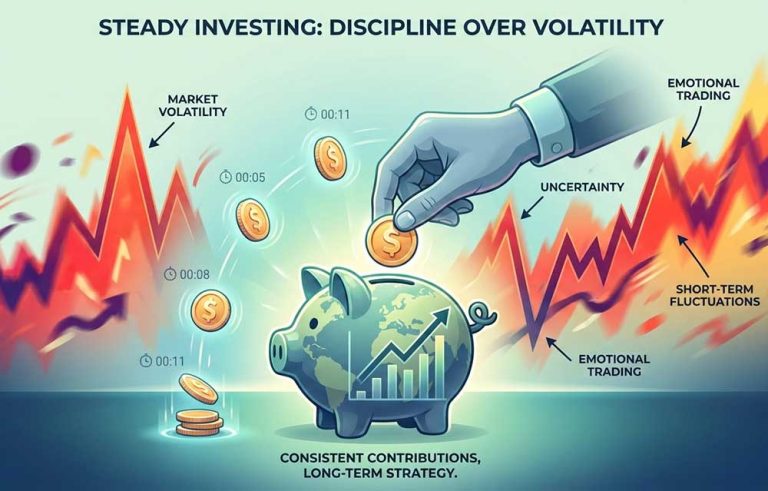

开始投资时,没人告诉你的是:投资最可怕的部分不是亏钱,而是等待那个永远不会到来的”完美时机R…

凌晨三点,林小姐盯着手机屏幕上那串数字,信用卡欠款58万,房贷还有120万,而她这个月的薪水只够还最低还款额的…

凌晨三点,小玲又失眠了。她盯着手机里的信用卡账单,五张卡的欠款加起来超过18万,这个数字像一座无形的大山压在她…

如果你有观察那些早已实现财务独立的人,你会发现一个奇特的现象:他们不炫耀名牌标志,不在晚宴上吹嘘投资成果,面对…

你是否曾经在深夜刷着手机银行,看着那几个数字,心里默默计算着离下个发薪日还有多久?或者在收到某笔“意外”账单时…

当你浏览财经新闻时,你会发现很多的标题都会提到“标普500”。你的同事炫耀自己的投资组合“跑赢了标普500”。…

当你推开一扇沉重的银行金库大门,冷冽的空气扑面而来。在昏暗的灯光下,你看到成堆的金条整齐码放,散发着永恒而冷漠…

还记得那个早晨吗?新闻头条像冰冷的雨水砸下来:“经济正式进入衰退期。” 你的心猛地一沉。仿佛脚下的地面突然变成…